Capital Construction Fund

The Merchant Maritime Act of 1936 created the CCF. It intended, like much of the New Deal of that era, to encourage building in U.S. shipyards and sailing with U.S. crews. The fund was to accumulate capital to build new ships, allowing the company to invest pretax earnings in an account and defer taxes on that income. The Capital Construction Fund (CCF) was a puzzle to me.

Locke Newlin said, “It was a farce. You could deposit pre-tax money and use it to build a ship. But this lost the cost basis in the ship, and there was no depreciation. This amounted to only a tax deferral, not necessarily a bad thing, but if you considered the alternative use of the money in the fund, there was no permanent gain.”

John Childs who worked in investment banking at Kidder Peabody for many years and was an expert in cash flow analysis. In the 1978 RJR annual report he wrote:

The laws which set the tone for United States maritime policy were written in 1916 and 1936. Today they are administered in an unrealistic fashion which fails to consider the changes that have reshaped world trade over the past sixty-two years. An archaic maritime policy, unevenly administered by a complex web of federal agencies, precludes the company’s efforts to achieve equal treatment. Needed are maritime laws countering the ominous predatory activity of not-for-profit Soviet shipping in U.S. trades. Other governments around the world are reformulating their policies on international shipping to reflect present-day realities.

These comments addressed other problems in the shipping industry, but they equally applied to the competitive disadvantage that Sea-Land had with its U.S. built ships and U.S. crews.

I cannot remember exactly why I met with John, but he quickly explained the less than obvious (at least to me) disadvantages of engaging in a CCF program. They were similar to those that Locke Newlin voiced. First was the opportunity loss on the money in the CCF that might have been invested elsewhere at a better return. Then there was a question of the temptation to “park” money in a CCF simply because it sheltered income from taxes now when there might be no need for more ships.

Sea-Land used the CCF for many years. In 1982, the balance sheet listed $31 million of cash as “Capital Construction Fund,” pending deposit in the fund.

Also, when the Navy bought the SL-7s for $268 million, these monies went into a CCF, deferring $101 million in tax. The money was to remain there until it could be used to build more ships. Such a program offered diminishing returns. The shipper could only avail itself of the CCF’s advantages if it wanted to build more ships.

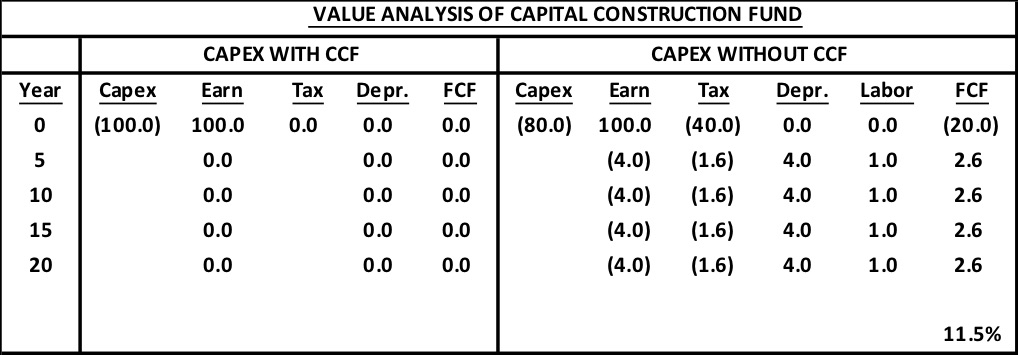

Comparing the CCF to other financing boils down to free cash flow. The CCF accounting is simple. An amount is put into the fund and used to build a ship. There is no income tax on the money put in the fund. There is no cost basis on the ship to be depreciated away (and used to shelter income from taxes over the twenty-year life of the ship.

Without the CCF, income tax would be due immediately on the earnings, 40% for example. The cost basis would be equal to the cost of the ship and would result in depreciation and tax savings over the twenty-year life of the vessel. As Locke Newlin pointed out, this is only a timing difference, the cash flows are the same, and the CCF appears to hold an advantage, except for the undefined opportunity cost.

However, the CCF imposes two other limitations – the ship must be built in a U.S. shipyard and manned by U.S. crews. If foreign construction and crews are cheaper, then those savings represent a return on not using the CCF. This example assumes that the ship can be built for only 80% as much in a foreign yard and that the foreign crew will save $1 million a year in labor costs. When these savings are factored in, the upfront taxes (an investment) gives an annual return of 11.5% over the life of the ship.

The CCF served as a warning about special deals underwritten by governments. A business that requires government subsidies to get an acceptable return is going to be a difficult business, subject to pressures from competitors who may not operate with the same restrictions.